EV Road Tax Structure in Malaysia –

How It’s Calculated & How Rates Are Different for Sedans and Non-Sedans

Source: paultan.org

As more electric vehicles (EVs) begin to make their way into Malaysia, it seems a good time to update readers on the vehicle road tax structure for these, given the official introduction of the BMW iX xDrive40 EV SUV earlier today and to clear up why its road tax is priced as it is.

In 2019, we published a story highlighting that the road transport department (JPJ) was set to move towards calculating the road tax rates for full-EVs (both motorcycles and cars) based on their motor kilowatt output instead of the traditional engine cc displacement as previously utilised. The switch to this has been made, as reflected by the road tax rates of EVs launched since then.

The rates of the new kilowatt-based road tax for private saloon motorcars were highlighted in that story, allowing calculations to be made for probable EV models for our market based on their kW output, and this has been established with great accuracy (as in the case of the Porsche Taycan, for example).

However, if you apply those specific rates for the iX xDrive40, the final calculation doesn’t match. Based on that table, it should be RM3,454, but the price list of the car states that the road tax is RM3,063, which is RM391 less.

So what gives? We reached out to JPJ, which said that the EV road tax rates are unchanged and follows that prescribed in the table, so there was nothing amiss on that front. As it turns out, the answer is simple enough. There is another set of road tax rates for other private vehicle types besides saloons (or sedans, if you will), which was not established in the story at that point.

The road tax rate for this differs from that for saloon motorcars, and completes the picture in establishing what the road tax will be EVs, based on their body-type. Before we head into a breakdown of the iX’s road tax, let’s recap the price structure of primary categories under the new kW-based system, including the one that wasn’t highlighted previously.

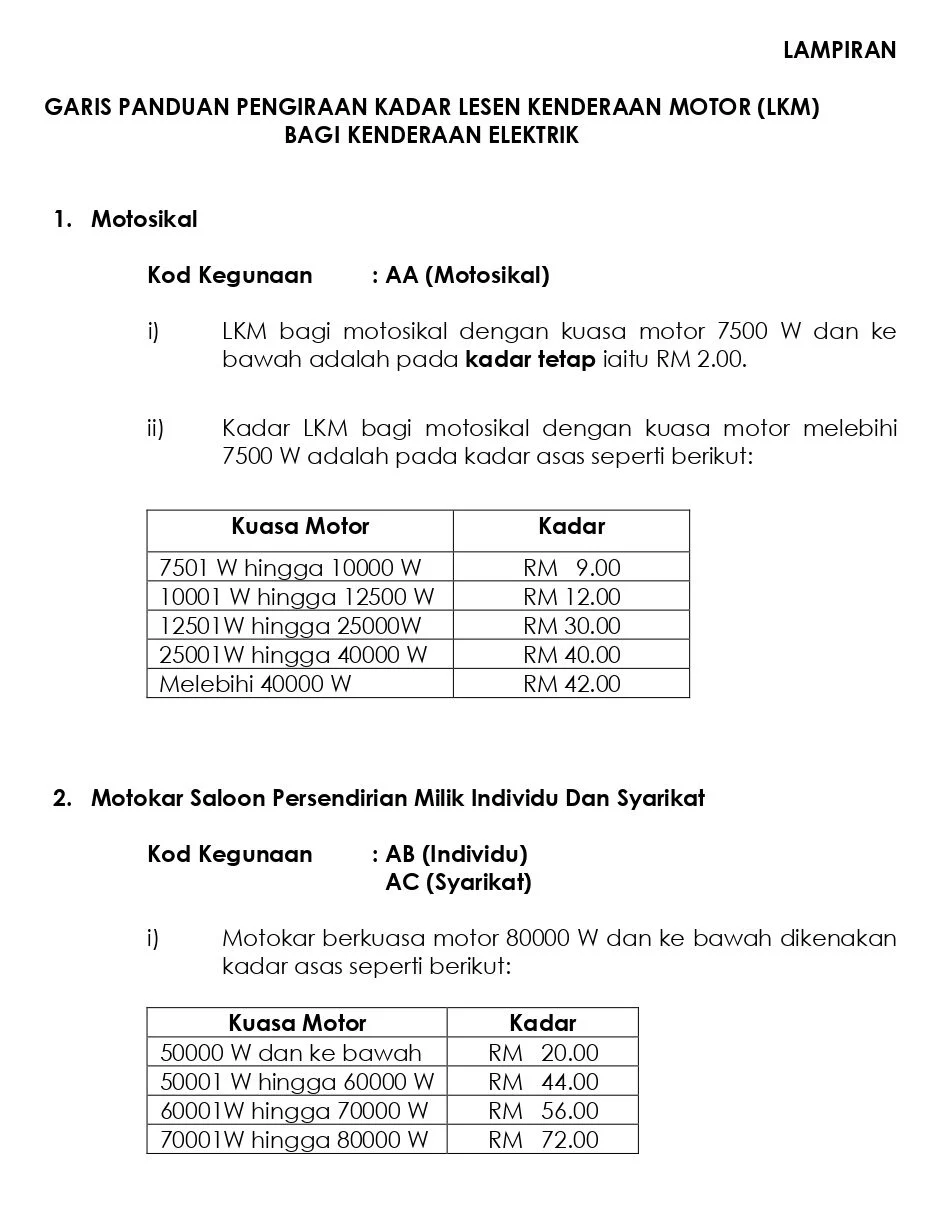

For electric motorbikes (code AA), the road tax for such two-wheelers with an output rating of 7.5 kW and below will be set at a fixed rate of RM2.

For e-motorcycles with a motor output rated above 7.5 kW, the rate is calculated as:

- Above 7.5 kW to 10 kW – RM9

- Above 10 kW to 12.5 kW – RM12

- Above 12.5 kW to 25 kW – RM30

- Above 25 kW to 40 kW – RM40

- For e-motorbikes with an output of above 40 kW – RM42

As for private saloon motorcars – individual (code AB) and company registration (AC) – with a rated output of 80 kW and below, the rates are as such:

- 50 kW and below – RM20

- Above 50 kW to 60 kW – RM44

- Above 60 kW to 70 kW – RM56

- Above 70 kW to 80 kW – RM72

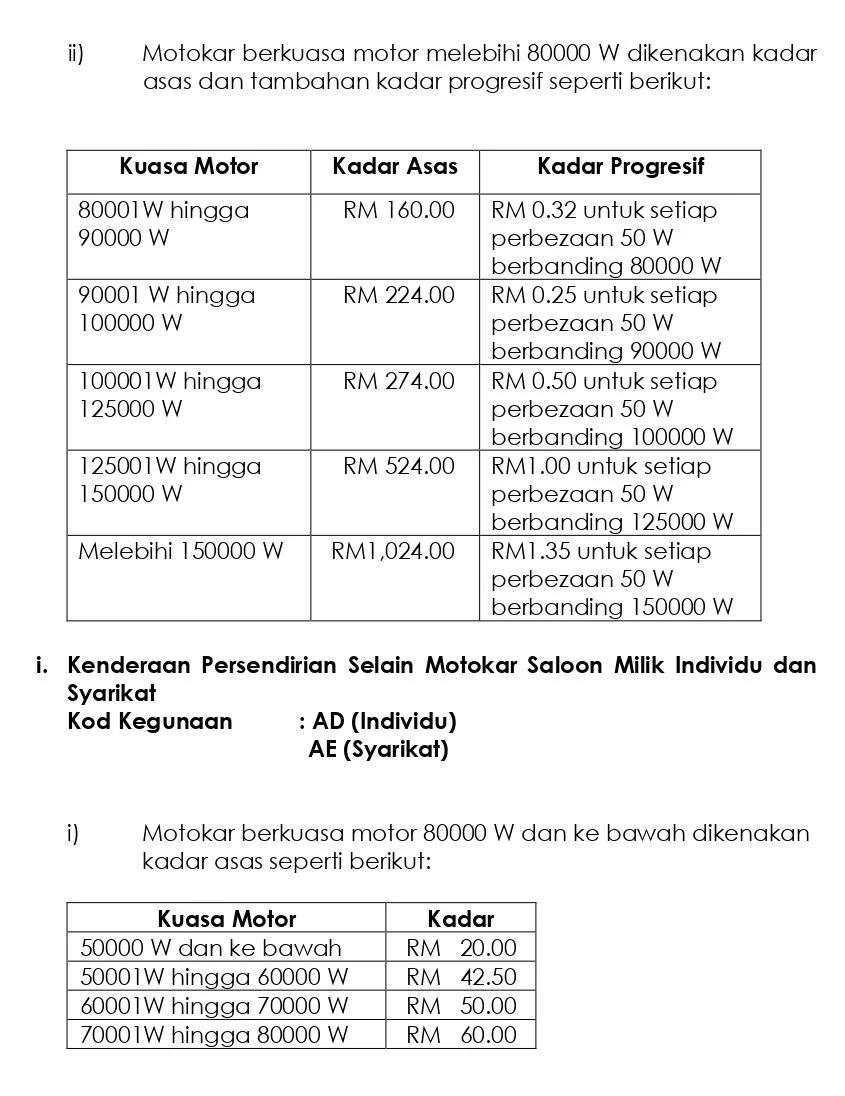

Vehicles with a rated motor output of above 80 kW will have a base road tax applied as well as a progressive rate calculated into the final sum. The road tax rate is calculated as follows, starting with a base rate and an additional rate for each kW increase:

- Above 80 kW to 90 kW – RM160, and RM0.32 sen for every 0.05 kW (50 watt) increase from 80 kW

- Above 90 kW to 100 kW – RM224, and RM0.25 sen for every 0.05 kW (50 watt) increase from 90 kW

- Above 100 kW to 125 kW – RM274, and RM0.50 sen for every 0.05 kW (50 watt) increase from 100 kW

- Above 125 kW to 150 kW – RM524, and RM1.00 for every 0.05 kW (50 watt) increase from 125 kW

- Above 150 kW – RM1,024, and RM1.35 for every 0.05 kW (50 watt) increase from 150 kW

Now, we come to the part missing initially. For private vehicles aside from saloon motorcars (like SUVs) – individual (code AD) and company registration (AE) – with a rated output of 80 kW and below, the rates are as follows:

- 50 kW and below – RM20

- Above 50 kW to 60 kW – RM42.50

- Above 60 kW to 70 kW – RM50

- Above 70 kW to 80 kW – RM60

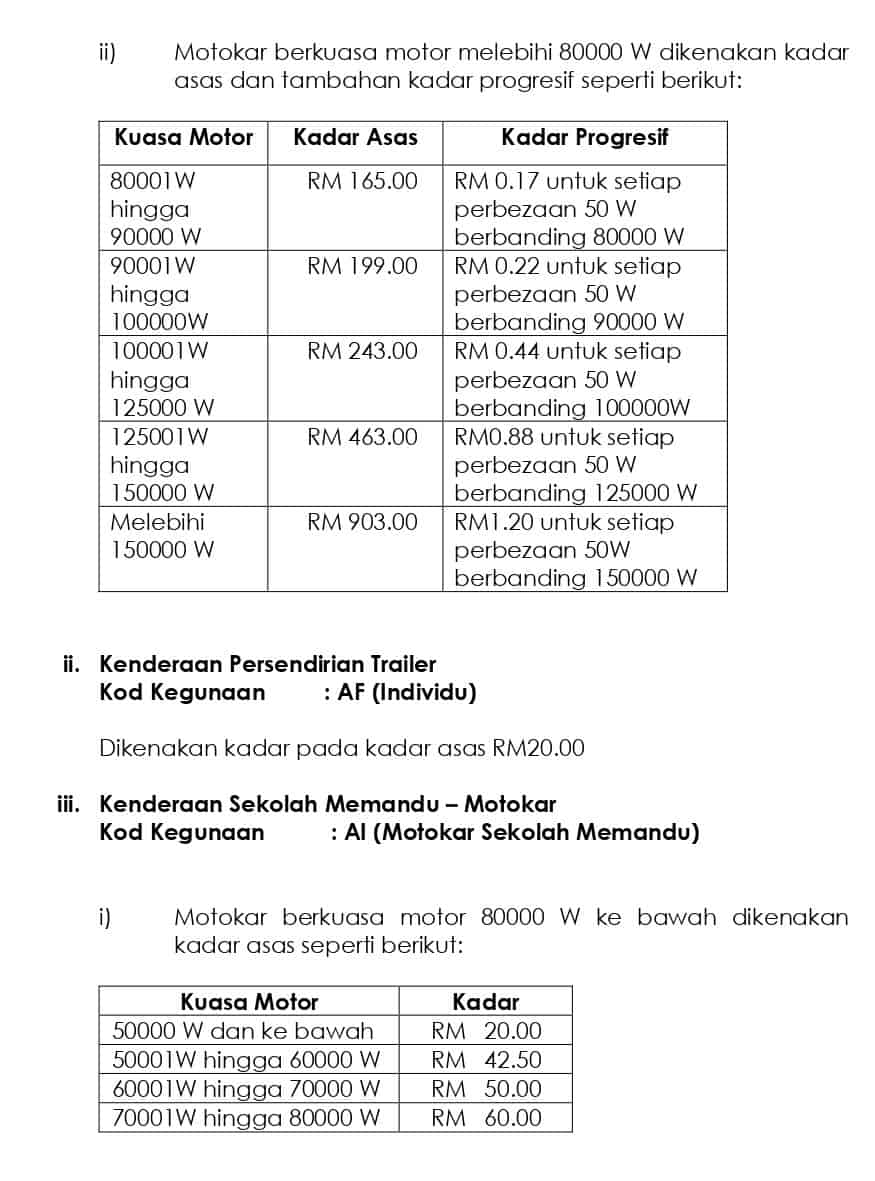

Vehicles in this category with a rated motor output of above 80 kW will have a base road tax applied as well as a progressive rate added into the final sum. The road tax rate is calculated as follows, starting with a base rate and an additional rate for each kW increase:

- Above 80 kW to 90 kW – RM165, and RM0.17 sen for every 0.05 kW (50 watt) increase from 80 kW

- Above 90 kW to 100 kW – RM199, and RM0.22 sen for every 0.05 kW (50 watt) increase from 90 kW

- Above 100 kW to 125 kW – RM243, and RM0.44 sen for every 0.05 kW (50 watt) increase from 100 kW

- Above 125 kW to 150 kW – RM463, and RM0.88 sen for every 0.05 kW (50 watt) increase from 125 kW

- Above 150 kW – RM903, and RM1.20 for every 0.05 kW (50 watt) increase from 150 kW

As you can see, the road tax rate for non-saloon private vehicles is lower from the baseline to above 150 kW (except in the 80 kW to 90 kW category, strangely, where it is RM5 more than for saloon-based EVs). Incidentally, this tax rate is shared with EVs used as driving institution vehicles.

With this, it’s easy to calculate the iX xDrive40’s road tax to that listed, which is not under the saloon category, but as non-saloon vehicle, given its definition as an SUV (it’s likely classified as jip – or jeep – under the department’s categorisation structure).

The iX xDrive40 has a 240 kW output. Based on the non-saloon rate, it pays RM903 (base rate up to 150 kw) and RM2,160 for the remaining 90 kW (at RM1.20 for every 50 watts more than 150 kW), which adds up to the RM3,063 road tax as printed.

Interestingly, the iX tax also highlights that the 50% road tax reduction for electric and hybrid cars announced by the PH government in 2019 may no longer be in place. Recipients of this incentive included the second-generation Nissan Leaf. The Leaf’s 110 kW motor meant that it would pay RM374 (RM274 base rate plus RM100 on the calculated increase from 100 kW) in road tax, based on the saloon motorcar rate. However, its road tax payable was RM187 when it was launched in July 2019.

Similarly, the Porsche Taycan also enjoyed the discounted rate at point of introduction here. For example, the Taycan 4S, with an output of 390 kW, has a road tax of RM7,504 (RM1,024 base rate plus RM6,480 as scaled on the 240 kW difference from 150 kW), but its payable road tax was RM3,752. It’s not known if this incentive is still in place.

There has of course been talk of zero road tax for EVs under the specific EV policy that will be announced by the government. The plan proposes the allowance for foreign automakers to bring in a number of completely built-up (CBU) units with zero excise and import duties (as previously reported), but also offering them full sales tax exemption and zero road tax. There is however no word on when the policy, which was supposed to have been unveiled in Q1 this year, will be announced.

Whatever the case may be, the full table now allows the calculation of EV road tax to be made for models sold here, according to vehicle type. As before, hybrids and plug-in hybrids (PHEV) will continue to pay road tax based on regular cc displacement for combustion engines, meaning there is no change no matter what kind of output their motors offer.